Little to Lose or Unprecedented Access?

What explains poorer Indian states’ extraordinary appetite for equity mutual fund investments?

Instead of looking for a needle in the haystack, buy the haystack. John Bogle- the father of Index MF investing; Credits: New York Times

“I have been investing INR5K monthly into these two equity SIPs. I hope to make 3x out of them in 20 years. I don’t think I will be able to make much money through my salary.” My cab driver remarked, while I was on my way to my office. That, and some data I had been looking at recently, sparked the idea for this essay.

Do investors from poorer states, with little legacy wealth, become more aggressive in their risk preferences because they have little to lose? Or is the easier access to riskier investments via digital brokerages/ fintechs making it easier for new investors from poorer states to sample them?

This issue builds on the idea that I have explored in my previous essay here, by looking at long-term trends in state-wise Mutual Fund (MF) allocations to answer these questions.

The Methodology

In this short note, I look at MF allocation in debt and equity schemes for Indian states grouped thematically in five baskets*

Rich Cohorts: States with GDP per capita > national average

Sophisticated- States with high levels of financial savings and awareness- Delhi (DL), Maharashtra (MH) and Gujarat (GJ)

Rich Agri- States with a high share of savings in agricultural land/non-financial instruments - Punjab (PB), Haryana (HR) and Andhra Pradesh (AP)

Other Southern States - Tamil Nadu (TN), Kerala (KL), Telangana (TG)

Then there are

Poor Cohorts: States with GDP per capita < national average

Convergent: States with GDP growth > national average - Uttar Pradesh (UP), Madhya Pradesh (MP), Rajasthan (RJ) and Assam (AS)

Laggards: GDP growth < national average - Bihar (BH), Jharkhand (JH), West Bengal (WB) and Chhattisgarh (CG)

So, who is the bravest of them all?

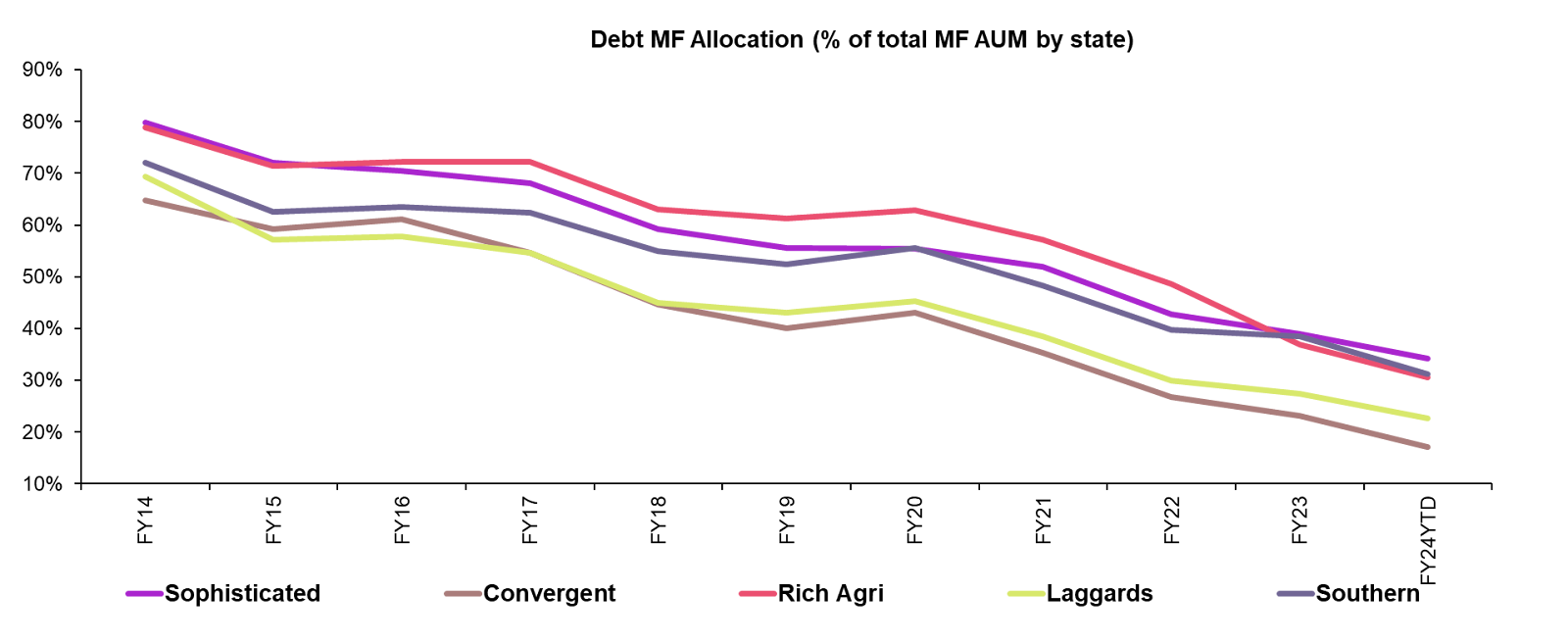

Illustration 1: Retail Debt MF allocation is at 1/3rd of its levels a decade ago. Bihar and Jharkhand have ~10% of total AUM in debt MFs. Source: AMFI, NSE

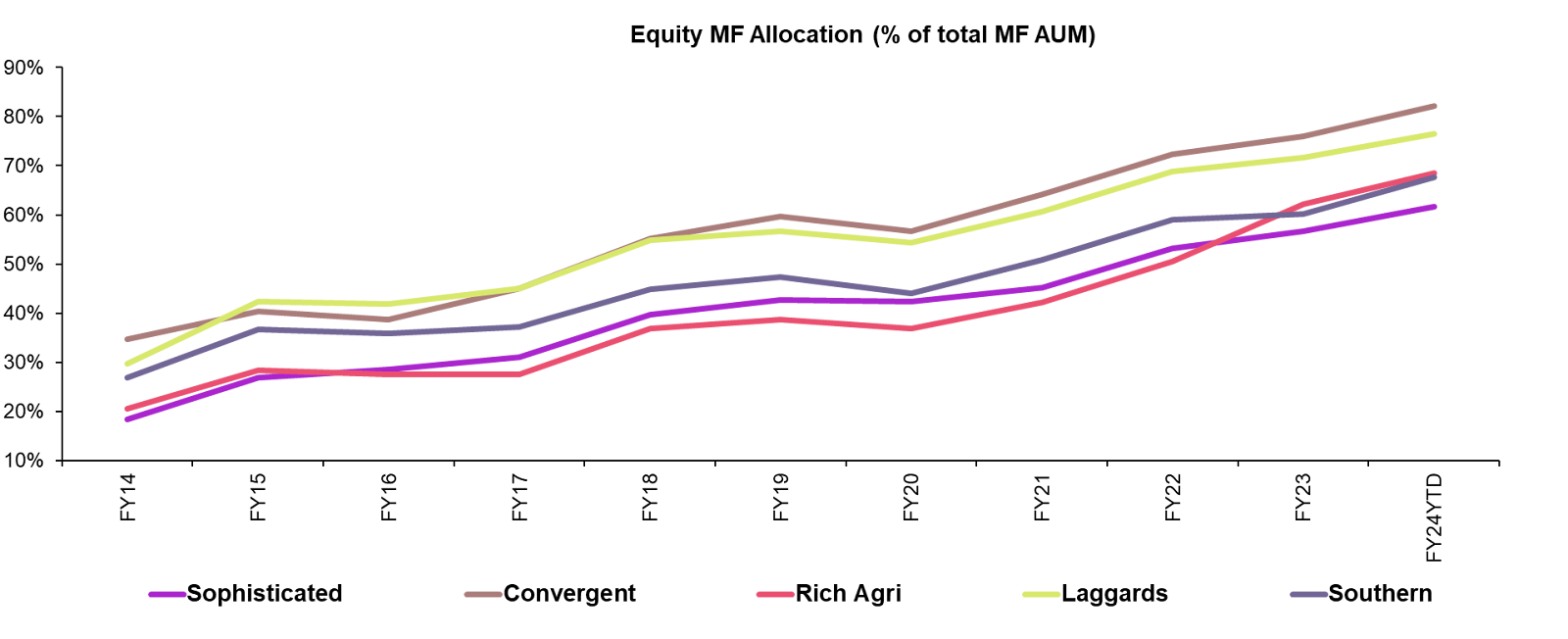

Illustration 2: Over the same period, and especially from FY20, equity debt MF allocations have risen by 3x, Source: AMFI, NSE

As Illustrations 1 and 2 show, there has been a general increase in risk appetite across states over the past 10 years, with the share of debt MF/ equity MF allocations falling/rising by ~3x over the period.

Moreover, data seem to corroborate the hypothesis that investors in Poor Cohorts have less to lose and hence seek greater risk – Convergent and Laggard states have seen a strong increase in equity MF allocation (at the expense of debt MF allocation).

Digging deeper, one finds that Poor Cohorts tend to have a higher allocation towards riskier equity MFs (i.e. a higher gearing for mid and small caps) compared to Rich Cohorts.

This further corroborates the hypothesis that investors with less to lose, and some disposable income at hand are more susceptible to “getting rich” quick asset allocations

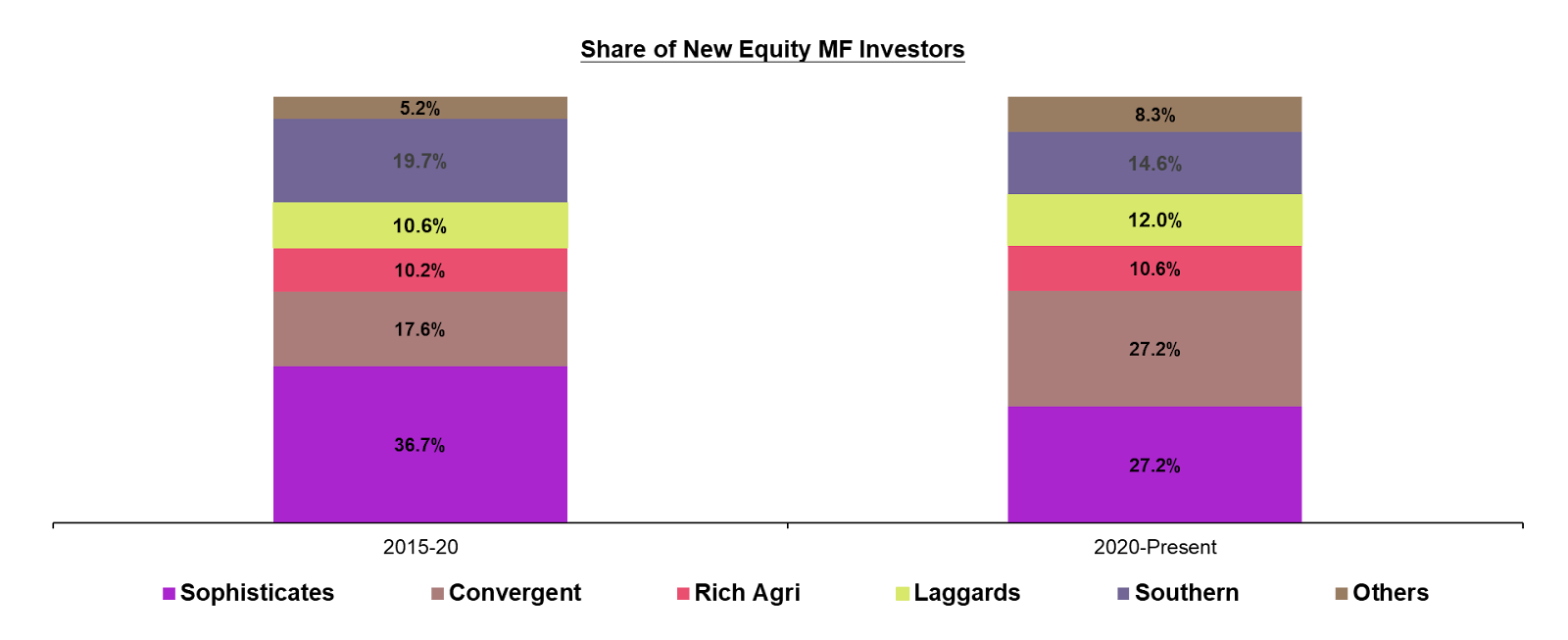

Illustration C: Share of new registered equity investors has risen dramatically in the Convergent States in the last 5 years; Source: AMFI,NSE

But that isn’t the complete picture. The differences in asset allocations across cohorts were less before FY18, even though regional disparities were the same. Much of the growth in new investors (Illustration C) and pivot towards riskier asset classes has been facilitated by better access to investing post Pandemic (See this essay for more).

For Invest-tech companies, this means two things.

First, rising incomes and (yet) existent regional economic disparities mean that newer investors will want to get rich quicker (higher appetite for stocks, options, equity schemes), translating into a greater SAM. Second, many of these will be small-ticket investors. The imperative will be on operational excellence, and an emphasis on basic investor education for category creation (like Nykaa did for beauty).